update on strategy and saylor

bitcoin bank

It’s been a minute since I’ve written anything, but want to build on the last few write-ups [1][2] regarding Saylor and MicroStrategy.

Will assume reader has familiarity with MicroStrategy (check out the prior write-ups if not!)

Since Oct 11, 2024 (when I published [1]), MSTR had gone up nearly 3x ($188 to $540) before coming down and settling in the low $300 range.

Saylor has done a lot since, changing the company name to Strategy, acquiring over 506,000 BTC, and issuing out two other preferred shares, STRK and STRF.

I’ve seen a lot of inaccurate takes with respect to how Strategy works, and wanted to boil down Saylor’s approach so folks can make a more accurate judgment on whether his financial alchemy is (or isn’t sustainable).

Very simply - Saylor’s approach is two fold:

Sell an option to purchase/convert MSTR shares where the strike (price to convert) ranges from +30% to +300% of the current price. Structure the sale to receive all the proceeds up front

This is done via convertible bonds and the STRK/STRF offering

Print more shares of MSTR when opportune/appropriate

This is done via the ATM offering

What isn’t explicitly stated is that Saylor has no intention of every paying back the principle / proceeds. His intention is to pay the interest expense for as long as it takes for MSTR stock to appreciate up until the relevant strike.

The beauty of this strategy is that Saylor effectively has created a ton of optionality that allows him to raise capital opportunistically:

Implied volatility high? Issue convertible bonds

Premium on Nav high? Sell MSTR shares via ATM offering

Neither? Issue out more preferred stock (STRK/STRF)

But what if Saylor blows up? Isn’t he taking on a lot of leverage?

If we just look at the facts:

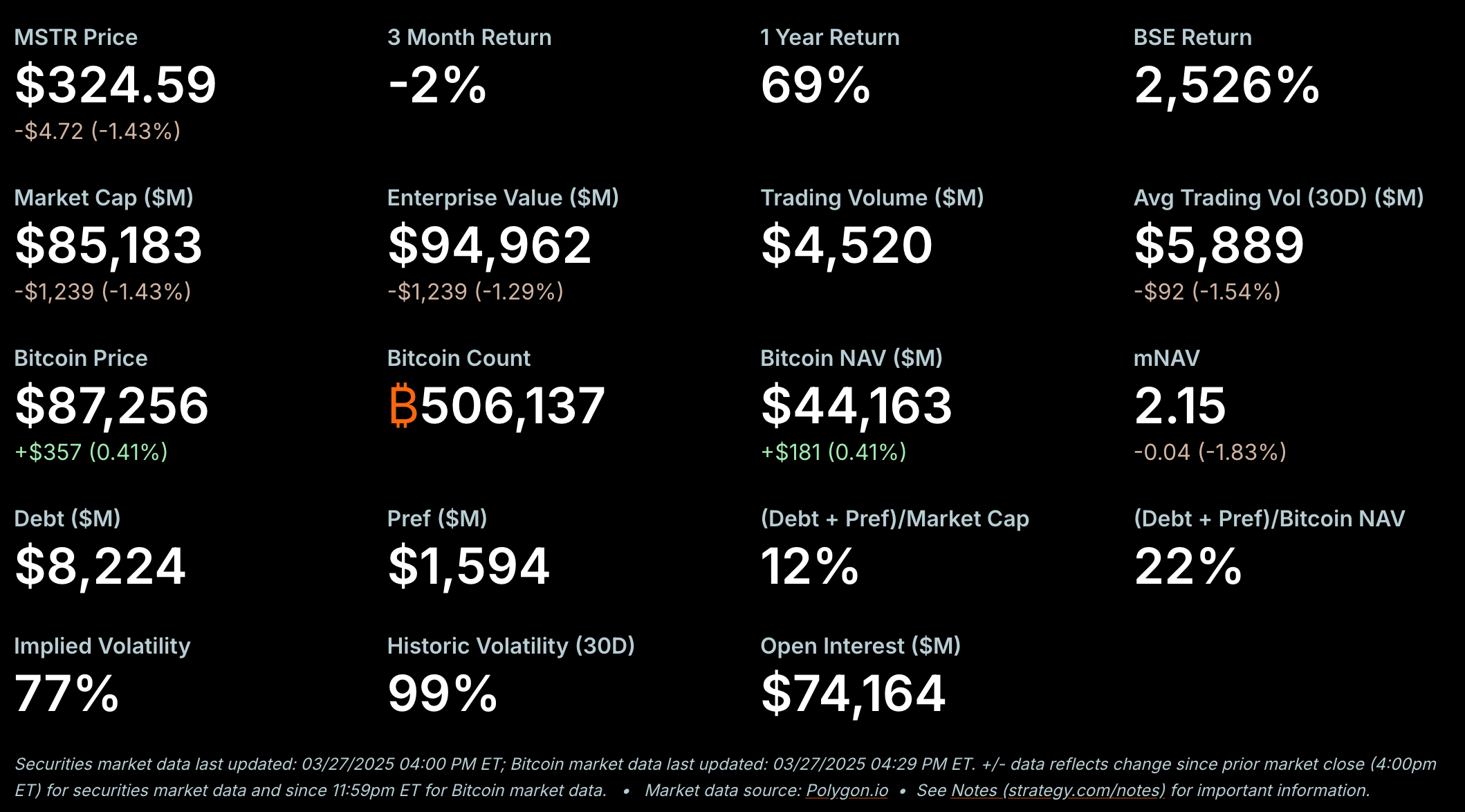

MSTR market cap is 85B and holds 506k BTC worth 44B

It has 8.2B in debt with a .421% annual coupon (34M in interest expenses)

58.4M for STRK and 85M for STRF in annual dividend payouts

If you play with the ratios - looking at debt / pref (pref is referring to the total marketcap of the preferred shares STRK/STRF) / interest expense relative to MSTR market cap and its net asset values, its very clear that Saylor has not taken on much leverage at all.

Another lens to view MSTR’s bitcoin treasury strategy is to draw a comparison to the traditional banks. Banks effectively:

Take deposits

Buy “safe” government backed debt (mortgage backed securities, t-bills, etc)

Pay you less than they get paid from the debt they purchase

To further juice returns, banks will lever up (fractional reserves). Occasionally, they fail.

The bitcoin treasury approach effectively:

Raise capital (take deposits)

Buy Bitcoin (instead of government debt)

Pay you in some form of MSTR stock and a routine coupon/dividend

However, the treasury company won’t (shouldn’t!) take as much leverage given the government won’t step in in the case where things go wrong.

In both cases, depositors make $ - banks pass through some fraction of the debt interest, the BTC treasury strategy passes through volatility (check this out on how this trade works exactly and why it is profitable for the convertible bond buyer).

The banks make $ from the net interest margin (difference between what the purchased debt pays and what they pass through) while the bitcoin treasury company makes $ from capital appreciation (or devaluation of the dollar relative to bitcoin).

The sustainability of this strategy really comes down to whether bitcoin continues to appreciate relative to fiat currencies.

At this point, Saylor is one of the biggest advocates and has been able to convert a number of different companies into taking a similar approach.

The price appreciation on MSTR and BTC have been the greatest selling point, and we’ve crossed the chasm to where the US government has adopted some form of a strategy reserve as well.

At this point, I think a very small percent of folks can understand and appreciate the approach that Saylor and Strategy has taken. As BTC and MSTR continues to do its thing, you will get more folks trying to understand the nuances around the btc treasury approach which just adds to the reflexivity and the sustainability of this.

Until next time

[1]

MSTR: Converting index investing into a BTC bid

I've previously written about MicroStrategy here. Check it out if you aren’t familiar with MicroStrategy and what Saylor has done to revamp the company.

[2]